In the realm of finance, understanding and managing loan risk is paramount for financial institutions. Loans, while essential for economic growth, also carry inherent risks that can impact the stability and profitability of lenders. This comprehensive guide delves into the intricacies of loan risk management, providing insights into its assessment, analysis, and mitigation strategies.

As we navigate the complexities of loan risk, we will explore key factors that contribute to it, delve into methods for analyzing loan portfolios, and uncover the significance of risk modeling and forecasting. We will also shed light on loan performance monitoring, restructuring, and workout strategies, equipping financial institutions with the tools to proactively manage at-risk loans.

Loan Definition and Risk Assessment

A loan is a sum of money borrowed from a lender, such as a bank or financial institution, that must be repaid with interest over a specified period of time. Loan risk assessment is the process of evaluating the likelihood that a borrower will default on their loan obligations.

This assessment considers factors such as the borrower’s credit history, income, and debt-to-income ratio.

Key Factors in Loan Risk Assessment

Several key factors are considered when assessing loan risk:

- Credit History: A borrower’s credit history provides insights into their past borrowing and repayment behavior. A history of missed payments or defaults can indicate an increased risk of default in the future.

- Income: A borrower’s income is a crucial factor in determining their ability to repay the loan. Lenders assess the borrower’s income stability, amount, and sources to ensure they have sufficient funds to cover the loan payments.

- Debt-to-Income Ratio: This ratio compares the borrower’s monthly debt payments to their monthly income. A high debt-to-income ratio can indicate that the borrower is already struggling to manage their existing debts, increasing the risk of default on the new loan.

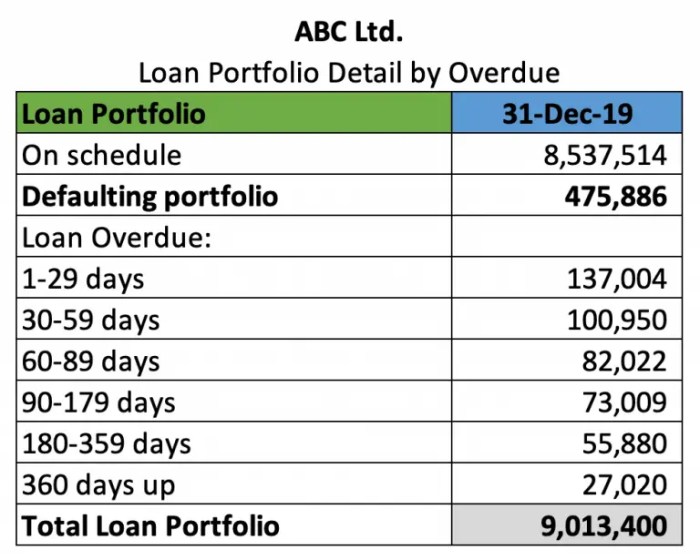

Loan Portfolio Analysis

A loan portfolio is the collection of loans held by a lender. It is crucial for lenders to assess the risk associated with their loan portfolios to ensure their financial stability and make informed decisions. Loan portfolio analysis involves identifying factors that contribute to loan risk and employing methods to analyze portfolios for potential risks.

Various factors can contribute to loan risk, including the borrower’s creditworthiness, loan terms, and economic conditions. Lenders can mitigate risk by diversifying their loan portfolios, setting appropriate interest rates, and conducting thorough credit checks on borrowers.

Methods for Analyzing Loan Portfolios for Risk

There are several methods for analyzing loan portfolios for risk, including:

- Historical analysis: Examining past loan performance data to identify patterns and trends that may indicate future risk.

- Scenario analysis: Simulating different economic scenarios to assess the impact on loan performance.

- Credit risk modeling: Using statistical models to predict the likelihood of loan default based on borrower characteristics and loan terms.

- Stress testing: Subjecting loan portfolios to extreme economic conditions to assess their resilience.

Risk Modeling and Forecasting

Risk modeling and forecasting are essential components of loan risk management. Risk modeling involves developing statistical or mathematical models to assess the likelihood and potential severity of loan defaults. These models use historical data and predictive analytics to identify patterns and relationships that can help predict future loan performance.

Risk Modeling Techniques

Various risk modeling techniques are available, including:

-

-*Logistic Regression

A statistical model that predicts the probability of a binary outcome (e.g., default or non-default) based on a set of independent variables.

-*Decision Trees

A tree-like structure that uses a series of binary splits to classify loans into different risk categories.

-*Neural Networks

Complex algorithms that can learn from data and identify non-linear relationships.

-*Monte Carlo Simulation

A stochastic technique that simulates multiple possible outcomes to estimate the probability distribution of loan performance.

Forecasting Loan Risk

Forecasting loan risk involves using historical data and predictive analytics to estimate the likelihood of future loan defaults.

This can be done through:

-

-*Time Series Analysis

Analyzing historical loan performance data to identify trends and patterns that can be used to forecast future defaults.

-*Scenario Analysis

Developing multiple scenarios based on different economic conditions or market assumptions to assess the impact on loan risk.

-*Stress Testing

Simulating extreme or adverse conditions to determine the resilience of the loan portfolio to potential shocks.

Loan Performance Monitoring

Regularly monitoring loan performance is crucial for financial institutions to identify and mitigate potential risks.

By tracking key indicators, institutions can detect early signs of financial distress and take proactive measures to prevent loan defaults.

Early Detection of At-Risk Loans

Early detection of at-risk loans is essential for minimizing losses. By identifying loans that exhibit warning signs, institutions can intervene early and implement strategies to mitigate risk, such as restructuring loan terms or providing additional support to borrowers. Timely intervention can prevent small issues from escalating into significant financial problems.

Loan Restructuring and Workout Strategies

Loan restructuring is a process of modifying the terms of a loan agreement to make it more manageable for the borrower. This can involve changes to the interest rate, the repayment schedule, or the amount of the loan. Workout strategies are plans developed by lenders to manage at-risk loans and prevent them from defaulting.

Loan Restructuring

Loan restructuring can be a viable option for borrowers who are facing financial difficulties and are unable to meet their loan obligations. The lender may agree to restructure the loan to make it more affordable, such as by reducing the interest rate or extending the repayment period.

Loan restructuring can help borrowers avoid default and improve their credit score.

Workout Strategies

Workout strategies are typically used when a borrower is in default or is at risk of defaulting on their loan. The lender may work with the borrower to develop a workout plan that will allow the borrower to repay the loan over time.

Workout plans can include a variety of measures, such as:

- Extending the repayment period

- Reducing the interest rate

- Forgiving a portion of the debt

- Modifying the loan terms

Workout strategies can be beneficial for both the lender and the borrower. The lender can avoid the costs associated with foreclosure and the borrower can keep their property and improve their credit score.

Risk Management Framework

Financial institutions must implement a robust risk management framework to identify, assess, and mitigate potential risks associated with loans. This framework should include:

- Risk Identification: Proactively identifying and categorizing potential risks based on loan characteristics, industry trends, and economic conditions.

- Risk Assessment: Evaluating the likelihood and potential impact of identified risks, assigning them appropriate risk ratings.

- Risk Mitigation: Developing and implementing strategies to reduce or eliminate risks, such as collateral requirements, loan covenants, and credit monitoring.

- Risk Monitoring: Regularly reviewing and updating risk assessments to reflect changes in loan performance, market conditions, and regulatory requirements.

Role of Technology in Risk Management

Technology plays a vital role in modern risk management frameworks, enabling:

- Data Analysis: Advanced analytics and machine learning algorithms can analyze large datasets to identify patterns and trends that indicate potential risks.

- Risk Modeling: Predictive models can simulate different scenarios and forecast potential loan losses, helping institutions make informed decisions.

- Automated Monitoring: Real-time monitoring systems can track loan performance and alert institutions to potential issues early on, allowing for timely intervention.

- Enhanced Risk Reporting: Technology facilitates comprehensive and timely risk reporting, providing insights for decision-making and regulatory compliance.

Impact on Financial Institutions

At-risk loans pose significant challenges to financial institutions, impacting their financial health, reputation, and compliance. These loans can lead to reduced profitability, increased loan loss provisions, and diminished investor confidence.

Regulatory and Compliance Implications

Financial institutions are subject to strict regulatory and compliance requirements regarding at-risk loans. Failure to adequately manage these loans can result in regulatory penalties, reputational damage, and even legal action. Institutions must comply with guidelines set by regulatory bodies, such as the Basel Accords, which establish capital adequacy ratios and risk management practices for banks.

Non-compliance can lead to fines, enforcement actions, and loss of licenses.

Best Practices for Managing Loan Risk

In the competitive world of finance, managing loan risk is paramount to ensure the stability and profitability of financial institutions. Industry best practices provide a roadmap for identifying, assessing, and mitigating loan risk, empowering lenders to navigate the complexities of credit risk management.

Identifying Loan Risk

Effective loan risk management begins with a comprehensive understanding of potential risks. Lenders should employ rigorous credit analysis techniques to evaluate borrowers’ financial health, including assessing their income, assets, liabilities, and credit history. Advanced data analytics and machine learning algorithms can supplement traditional methods, providing deeper insights into borrowers’ risk profiles.

Assessing Loan Risk

Once loan risks are identified, lenders must assess their severity and likelihood. Quantitative risk assessment models, such as credit scoring systems and stress testing, assign risk ratings to borrowers based on historical data and economic forecasts. Qualitative assessments, involving expert judgment and industry knowledge, complement quantitative models to provide a holistic view of loan risk.

Managing Loan Risk

Managing loan risk involves implementing strategies to mitigate potential losses. Diversification of loan portfolios across different borrowers, industries, and geographic regions reduces concentration risk. Setting appropriate loan-to-value ratios and collateral requirements ensures that lenders have sufficient protection in case of default.

Risk-based pricing, where borrowers with higher risk profiles pay higher interest rates, incentivizes prudent borrowing behavior.

Successful Risk Management Strategies

Banks and financial institutions worldwide have successfully implemented best practices for managing loan risk. For instance, Citigroup’s Comprehensive Credit Risk Management System utilizes advanced analytics and predictive modeling to identify and mitigate loan risks. Wells Fargo’s Risk Management Framework employs a combination of quantitative and qualitative assessments to ensure the soundness of its loan portfolio.

These strategies have contributed to the resilience of these institutions during economic downturns and periods of financial instability.

Emerging Trends in Loan Risk Management

In the rapidly evolving financial landscape, loan risk management is undergoing a significant transformation. Emerging trends, such as artificial intelligence (AI) and machine learning, are revolutionizing the way financial institutions assess, mitigate, and manage loan risks.Data analytics and predictive modeling are becoming increasingly important in loan risk management.

By leveraging vast amounts of data, institutions can gain deeper insights into borrower behavior, identify potential risks, and make more informed lending decisions.

AI and Machine Learning

AI and machine learning algorithms can analyze complex data patterns and identify hidden relationships that may not be apparent to human analysts. This enables institutions to automate risk assessment processes, improve accuracy, and make more precise predictions about loan performance.For

instance, AI-powered systems can analyze historical loan data, borrower demographics, and economic indicators to predict the likelihood of loan default. This information can be used to adjust loan terms, set appropriate interest rates, and allocate capital more effectively.

Case Studies and Real-World Examples

Delve into case studies that illuminate the complexities of loan risk management. Witness how financial institutions navigate the challenges and embrace innovative strategies to mitigate risk.

Success Stories

- Case Study: Bank of America’s Risk Management Framework: Bank of America implemented a comprehensive risk management framework that leveraged data analytics and scenario modeling to identify and mitigate loan risks. This proactive approach led to a significant reduction in non-performing loans and enhanced financial stability.

- Case Study: Citigroup’s Predictive Modeling: Citigroup developed sophisticated predictive models to assess loan risk. These models incorporated a wide range of data sources, including credit history, financial ratios, and market conditions. The models enabled Citigroup to identify potential problem loans early on and take proactive steps to minimize losses.

Learning from Failures

- Case Study: Subprime Mortgage Crisis: The subprime mortgage crisis of 2008 exposed the consequences of inadequate loan risk management. Lenders approved loans to borrowers with poor credit histories and low down payments, leading to a surge in defaults and foreclosures. This crisis highlighted the importance of thorough credit analysis and risk assessment.

- Case Study: Wells Fargo’s Cross-Selling Scandal: Wells Fargo employees pressured customers into opening unnecessary accounts and products. This aggressive sales culture resulted in reputational damage, regulatory fines, and a loss of customer trust. It emphasized the need for ethical lending practices and robust risk management systems.

Final Conclusion

In conclusion, loan risk management is a multifaceted and dynamic field that requires a comprehensive understanding of financial markets, risk assessment techniques, and regulatory frameworks. By adopting industry best practices, leveraging emerging technologies, and fostering a culture of risk awareness, financial institutions can effectively mitigate loan risk, safeguard their financial health, and contribute to the stability of the financial system as a whole.

FAQ Section

What are the key factors that contribute to loan risk?

Factors that contribute to loan risk include borrower creditworthiness, loan purpose, collateral value, loan terms, and economic conditions.

How can financial institutions analyze loan portfolios for risk?

Loan portfolio analysis involves assessing the risk profile of individual loans and the portfolio as a whole, using techniques such as credit scoring, cash flow analysis, and stress testing.

What is the role of risk modeling in loan risk management?

Risk modeling involves developing statistical models to predict the probability of loan default. These models incorporate historical data, economic factors, and borrower characteristics to estimate loan risk.

How can financial institutions monitor loan performance?

Loan performance monitoring involves tracking key indicators such as payment history, loan-to-value ratio, and debt-to-income ratio to identify potential problems early on.

What are some workout strategies for managing at-risk loans?

Workout strategies for at-risk loans include loan restructuring, forbearance, and debt settlement, aimed at finding a mutually acceptable solution for both the borrower and the lender.

{kind=link}